Grain Report Friday - 03rd February

- Clear Grain Exchange

- Feb 3, 2023

- 2 min read

Our goal is to help growers and their agents determine the selling price for their grain by providing relevant price discovery each day. Check out the moves in overnight international markets and yesterday's actual traded prices across Australia. There's also market commentary giving context and comparisons to prices of international physical markets. If you need to change your offer price, simply edit it before market open.

What price do you want for your grain?

Look Out!

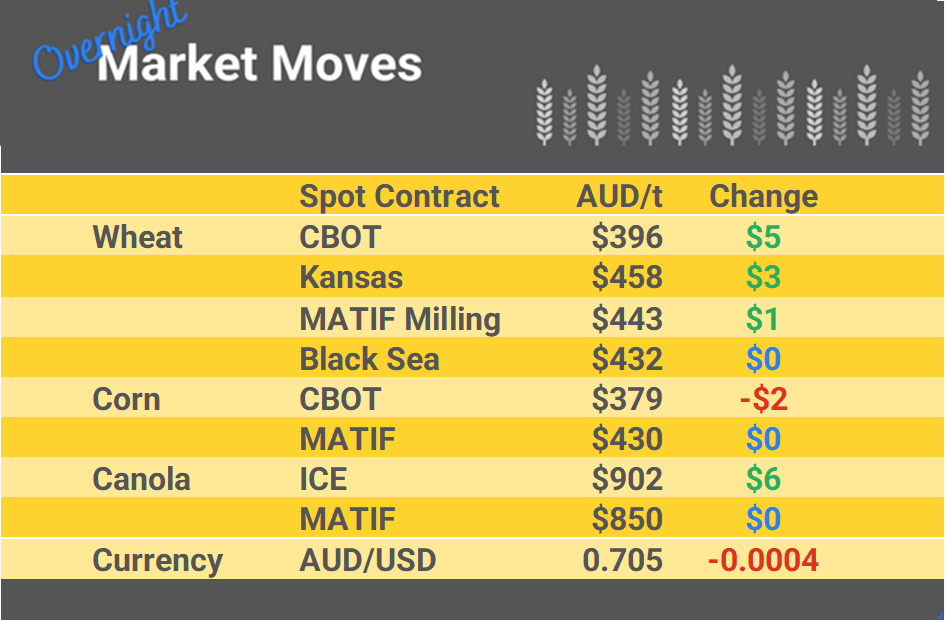

Markets mixed with Kansas wheat and corn off and beans up.

The AUD is hovering around the 71 cents mark.

The US Ag Attaché’ has come out and forecast the Argie Bean crop 36 million tonnes, which is almost 10 million tonnes under what the USDA called it in the last World Agriculture Supply and Demand Estimate Guess (WASDE).

There is rain forecast for Argie over next 10 days, which will see the markets breathe a slight sigh of relief.

In Brazil, the bean harvest is off to a slow start at 5% harvest versus 12% for the same time last year and the weather forecast is for rain and cool weather, which will slow down harvest further.

Brazil, who will grow around 150 million tonnes of soybeans this year, up 20 million tonnes from last year, needs the world's largest lung, as the vegan’s sip their soy lattes and eat their plant based protein burger, condemning cows for breathing out too much greenhouse gas.

However, whilst world bean production is up 30 million tonnes this year, world stocks of beans are only forecast to be up 5 million tonnes from last year to 103 million tonnes. If the USDA knocks the Argie crop back 10 million tonnes, as the US Ag Attaché’ is now forecasting, then suddenly, this balance sheet goes from bearish to bullish (higher oilseed prices).

The South Koreans bought another 60,000 tonnes of feed wheat, paying USD $339.60 per tonne C&F (Cost and Freight) for June shipment.

It's a multi origin sale, that could come from several origins, but likely to come from Aus.

This sale was done at USD $0.07 lower than the business done on Tuesday; pull my pants down and tap me on the shoulder.

It works back to the same level FIS (Free In Store) WA at the AUD $420 mark, and Track $395 East Coast.

The Gypos are also in the tender process with 20 offers, with the lowest being the Ruskies at USD $322.80 C&F. This is around $14 lower than last tender on 12th of Jan.

Some of this price drop is attributed to ocean freight softening.

Most importantly we're always here to help!

Please give us a call or email if you have any questions.

Call 1800 000 410 or Email support@cgx.com.au

Comments